|

|

A Tougher Third Quarter

Editorial

Jul 4, 2014 2:05 AM

By Avi Krawitz

|

|

|

RAPAPORT... The second quarter was always going to be a quieter period for the diamond trade. Therefore, few were surprised that the RapNet Diamond Index (RAPI™) for 1-carat diamonds softened during the period, as reflected in the Rapaport Monthly Report – July 2014. This time of year is traditionally a slower period for the market, despite the fairly busy trade show schedule.

In the coming months, things will likely get worse before they get better. The third quarter tends to bring sharper declines before demand typically improves closer to the holiday season, when prices subsequently firm up. There is a cyclical nature to the diamond trading calendar that partly explains the current slowdown, and the almost positive mood that lingers is a reflection of the true strength of the first quarter that preceded the quiet.

The first quarter saw the strongest quarterly growth since the second quarter of 2011. Prices rose and demand increased during the first three months of the year due to inventory replenishment following the Christmas and Chinese New Year seasons. In fact, the increases were far healthier and more sustainable than three years ago, which has encouraged the skeptics.

Back in 2011, the sharp price growth experienced in the first half of the year was largely driven by market speculation. Conversely in 2014, first quarter growth reflected steady demand filtering in from the retail sector. The U.S. Christmas shopping season was fairly robust and the Chinese New Year signaled that the market in China is still growing, even if it’s doing so at a slower pace.

The diamond market has been cautious since 2011, having learned its lesson from the speculative bubble that ultimately burst back then. Today, diamond wholesalers and manufacturers are managing their inventory in a far more efficient and leaner manner. This was evident in the second quarter of 2014 when they scaled back their buying and avoided pushing prices higher in the market when it was not warranted.

Therefore, dealers recognize that there’s no reason to panic just yet as 2014 has been a relatively good year so far in terms of turnover. It has been less so, however, when measuring profitability. Tight liquidity and high rough prices continue to impact dealer-to-dealer trading and market sentiment.

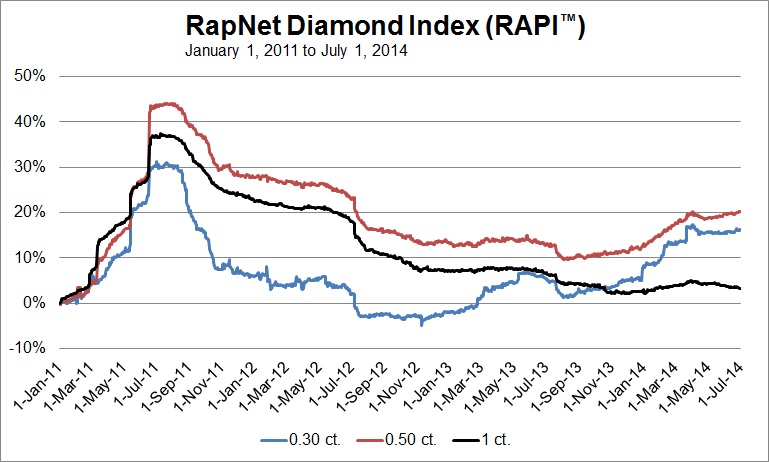

Manufacturers are also wary of the fact that 1-carat diamond prices have been in a measured but consistent decline since 2011 (see graph). Other categories have performed better as the market has become more selective amid economic uncertainty. In particular, 0.30-carat to 0.50-carat certified diamonds have been strong growth points for the trade in the past two years as Chinese consumers matured and shifted to smaller and lower-quality goods. Similarly, demand for SI-clarity goods has been strong.

RAPI is based on the average asking price in hundred $/ct. for the top 25 quality round diamonds (D-H, IF-VS2, RapSpec-2 and better) with GIA grading reports offered for sale on RapNet – Rapaport Diamond Trading Network.

However, demand even for these goods slowed in the second quarter. RAPI for 0.30-carat diamonds fell 0.8 percent, while RAPI for 0.50-carat goods increased a slight 0.2 percent. Rough prices meanwhile were basically stable and Rapaport estimates that average rough prices increased by about 7 percent in the first half of 2014.

Manufacturers continue to seek out alternative ways to garner profit. For many, it’s preferable to buy polished and resell than to buy rough and manufacture. Manufacturers, frustrated by the long turnaround time for grading diamonds at the Gemological Institute of America (GIA), are also opting to sell more non-certified 0.30-carat goods in parcels. In that way, they avoid the very long wait for grading and the associated additional expense.

However, not everyone can do this as manufacturing rough and certifying polished remains the core business of the diamond trade. Despite the backlogs, the intake at the various labs continues to increase – as do listings of certified goods on RapNet – the Rapaport Diamond Trading Network.

Therefore, the market has reached a position where there are a lot of goods in the pipeline but relatively weak demand that might not fully support this supply. In fact, if the GIA were to suddenly increase its turnover, there could be an oversupply of diamonds on the market, which would influence prices to drop further. In that sense, the GIA backlog is actually regulating the market.

Currently, the backlog is focused on pointer-size diamonds whereas the GIA has improved its turnaround time for 1-carat diamonds. While grading reports for goods below 1-carat are taking at least four months for the GIA to process, 1-carat to 3-carat goods are taking four to six weeks.

A larger supply of 1-carat diamonds in the market may be one of the factors that influenced softer prices for these goods in the second quarter, and particularly in June. Certainly, there has been an increase in the volume of 1-carat diamonds listed by suppliers on RapNet in the past month. With more goods on the market and no sudden burst of demand expected, the downtrend is unlikely to reverse in the third quarter. At best, the market will remain stable.

In such an environment, a prolonged downturn going into the third quarter places additional pressure on manufacturing profit margins. If polished prices are not rising, manufacturers will reduce their demand for rough. Whether that will translate to lower rough prices remains to be seen.

The major mining companies, which are working within more corporate-like structures than a year ago, are faced with their own rising costs and have more ambitious targets to meet for shareholders. De Beers and ALROSA will therefore not lower their prices in a hurry.

If they’re able to maintain stable rough prices, they could break the cyclical nature of diamond trading in 2014. After all, it was the decline in rough demand and prices during the third quarter of 2013 that enabled better profit margins from the resulting polished sold at the beginning of this year.

However, manufacturers were still conscious in the first quarter of 2014 that polished prices would have to rise further if they were to garner some profit later in the year. After all, that new higher-priced rough would come to market as polished in four months’ time. Today, four months later, polished prices did not increase but softened, and the lack of profitability remains the number one concern among dealers and manufacturers.

True enough, sentiment is relatively positive in the diamond industry at the start of the third quarter, given the current environment. The JCK Las Vegas show, while not at all spectacular, reassured the industry that U.S. demand is stable, and the disappointing Hong Kong show was more a reflection of a superfluous show than a dire market.

However, the mood is changing as the diamond market’s cyclical nature roles on. While the trade may expect the weak polished market to continue during the third quarter, conditions would be unsustainable if it lacks a parallel decline in the rough. Manufacturers will reduce their rough buying in an attempt to force through reduced prices.

They recognize that the volume of business done is secondary to the amount of profit they’re able to garner. Therein lays the true challenge for the trade as the toughest part of the cycle begins.

The writer can be contacted at avi@diamonds.net.

Follow Avi on Twitter: @AviKrawitz and on LinkedIn.

This article is an excerpt from a market report that is sent to Rapaport members on a weekly basis. To subscribe, go to www.diamonds.net/weeklyreport/ or contact your local Rapaport office.

Copyright © 2014 by Martin Rapaport. All rights reserved. Rapaport USA Inc., Suite 100 133 E. Warm Springs Rd., Las Vegas, Nevada, USA. +1.702.893.9400.

Disclaimer: This Editorial is provided solely for your personal reading pleasure. Nothing published by The Rapaport Group of Companies and contained in this report should be deemed to be considered personalized industry or market advice. Any investment or purchase decisions should only be made after obtaining expert advice. All opinions and estimates contained in this report constitute Rapaport`s considered judgment as of the date of this report, are subject to change without notice and are provided in good faith but without legal responsibility. Thank you for respecting our intellectual property rights.

|

|

|

|

|

|

|

|

|

|

Tags:

Alrosa, Avi Krawitz, De Beers, diamonds, GIA, Jewelry, Rapaport

|

|

|

|

|

|

|

|

|

|

|

|

|