|

|

The Next Diamond Decade

The Roaring ’20s

Dec 25, 2019 8:15 AM

By Avi Krawitz

|

|

|

RAPAPORT... It wasn’t that long ago that De Beers declared the 2010s “The Diamond Decade.” Growth in China and India was projected to drive demand, while the US would take small steps out of recession. This is what Varda Shine, then-head of De Beers’ supply arm, the Diamond Trading Company (DTC), predicted in a 2010 interview with Rough & Polished.

In some sense, she was correct. The last 10 years have seen the Chinese consumer emerge as an influential force in the diamond industry. At times, that has been to the trade’s advantage. In 2010 to mid-2011, for instance, jewelers like Hong Kong-based Chow Tai Fook and Luk Fook accelerated their expansion into mainland China, prompting an aggressive and arguably speculative surge in polished prices.

During other periods, however, China’s influence on the trade has been more volatile. Post-2011, growth slowed; jewelers recognized that their expansion had been too aggressive, leaving them with too much inventory. There was also the anti-corruption campaign that President Xi Jinping waged at the start of his premiership, which curbed luxury purchases. And more recently, the US-China trade war has made both consumers and the industry more cautious.

These events have affected diamond demand, particularly for 0.30- to 0.50-carat goods, which are strong items in China.

Shine was also correct in her assessment of the US, which continues to be the mainstay market for the diamond industry. Overall, global diamond jewelry sales grew 16% from an estimated $65.3 billion in 2010 to $76 billion in 2018, according to De Beers.

A turbulent trade

Despite the rise in diamond jewelry demand, the decade has been characterized more by turbulence in the trade. The midstream has struggled with low manufacturing profitability, tight liquidity, reduced bank credit, changing consumer habits and retail strategies, and a lack of balance between supply and demand.

The 2008 financial downturn led to greater compliance requirements from financial institutions, which in turn led to reduced bank credit. The result was that manufacturers had to start self-financing more of their rough purchases, which they continued to make even as mining companies maintained high price levels relative to what cutters were getting for polished.

Just as jewelry retailers were becoming more prudent about buying polished for inventory, three new mines came onstream in 2017, raising supply to pre-2008 levels and overstocking the midstream. Polished prices slumped in that environment, with the RapNet Diamond Index (RAPI™) for 1-carat diamonds declining 17.7% from January 1, 2010, to press time on December 25, 2019.

Meanwhile, millennial consumers emerged as the core engagement-ring customers, and their embrace of technology effected a dramatic shift in retailers’ marketing and selling methods.

Change is the only constant

The silver lining is that the industry has made significant moves in the past two to three years to help it navigate the volatility that still lies ahead. Perhaps most notably, it is embracing technology to improve efficiency — and businesses at every stage of the pipeline will need to be more efficient if the industry is to grow amid all the changes yet to come. The industry will look very different in 10 years from now.

Here, we make 10 predictions of how the market will evolve in the 2020s, though perhaps they’re better read as suggestions for what needs to happen to ensure growth. Either way, we’re optimistic that it will be better than the 2010s, perhaps even an era that’s worthy of the title “The Diamond Decade.”

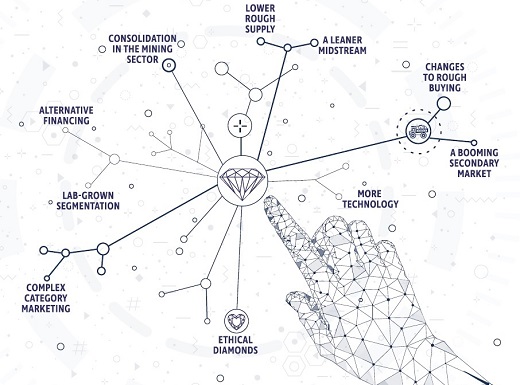

1. Lower rough supply

Mining companies currently have a lot of rough inventory that didn’t sell in 2019. The Rapaport Research Report has expressed concern that they may push these goods to the market in the coming year and thus prolong the midstream’s oversupply struggles in the short term. However, mining production has peaked, and we expect rough supply to diminish over the next five to 10 years as several key mines shut down.

Argyle is set for closure in 2021, Ekati in 2023, and Diavik in 2025. That will take about 25 million carats of annual production off the market in the next five years alone, based on 2018 production at those mines. Operations set to run dry by 2030 include the 6 million-carat-per-year Gahcho Kué mine and the Renard mine with its 2 million carats a year.

The shortfall in the supply of new rough, combined with growing demand out of the US, China and India, should support polished prices in the coming decade.

2. Consolidation in the mining sector

A drop in rough supply bodes well for the major miners — particularly Alrosa, which, in our opinion, has the strongest production resources. However, the smaller miners are expected to struggle as mining costs rise and the economics of developing a diamond mine become tighter. Already, we’ve seen operations such as Trans Hex and single-asset miners like Firestone Diamonds and Stornoway Diamond Corp. having trouble staying afloat. Mines that were feasible 10 years ago when the development decision was made are no longer viable at current prices. More junior miners will likely drop off the market, and only those companies with high-volume production and better value grades will survive.

3. A booming secondary market

As rough supply declines, recycled jewelry will become an increasingly important source of diamonds. Rapaport has already projected its confidence in estate jewelry and has also been engrossed in the secondary market, holding auctions of recycled diamonds over the last five years.

We expect these markets to grow in the coming years as baby boomers get older and seek to liquidate high-value assets that appeal to millennials for their uniqueness and the ethical assurances they offer. Furthermore, China will become a resource of recycled diamonds as the market there matures.

4. Changes to rough buying

Over the next decade, the midstream is expected to become more efficient, and manufacturers will aim to produce polished according to demand. The first stage of implementing that strategy will be at the rough-buying level.

Manufacturers want to reduce their stock of hard-to-sell goods, so they’ll only be purchasing the rough they need to fill polished orders. We expect purchasing on demand to become the preferred method of buying rough, with systems such as Lucara’s Clara platform gaining traction. That will put pressure on De Beers and Alrosa to adjust their respective contract systems in the longer term.

5. A leaner midstream

The manufacturing sector is likely to get smaller in the coming years, either through mergers or as nonprofitable businesses close. Large-scale operators will gain market share, and specialized niche cutters will find their space.

Dealers, too, are being squeezed, with “everybody’s supplier’s supplier trying to sell to the customer’s customer,” as Rapaport Chairman Martin Rapaport noted in a recent presentation.

But that model is not sustainable. Miners are best skilled at mining, manufacturers at cutting and polishing, and retailers at selling. Dealers, therefore, will be able to restore their relevance by capitalizing on their middleman role: connecting the various segments of the market and providing retailers with, as Rapaport put it, “the right goods at the right time [and] the right price.”

6. Alternative financing

Traditional banks, most notably in India, will continue to pull away from financing the diamond trade. At the same time, new instruments will become available and gain acceptance, offering alternative methods of financing. Examples include equity- or collateral-based loans, cryptocurrency token exchanges, and even crowdfunding.

These alternatives won’t completely replace the lost bank credit, but they will help alleviate midstream liquidity concerns. Overall, the trade’s diminished reliance on bank credit will feed into its drive for efficiency.

7. More technology

Technology will play a bigger role in streamlining the manufacturing process, with artificial intelligence (AI) becoming increasingly important in automating diamond cutting and grading. That will result in some jobs becoming redundant and some changing, but the added value is that it will shorten the time it takes a diamond to travel from mine to market. The midstream will further embrace technology in its sales platforms, tying into the various blockchain programs to show proof of origin.

Retailers will also make greater use of technology, with an emphasis on omni-channel — the interplay between online and in-store sales options. Jewelers that can tap into suppliers’ virtual inventory — which will need to feature good images and transparent details — will be able to offer a better, sleeker shopping experience for consumers. And for the supplier, providing such services will become as important as the diamonds it sells, if not more so.

8. Ethical diamonds

Responsibly sourced diamonds will be clearly differentiated from those that are not, and brands will be willing to pay a premium for the former. The conversation around ethics in the last decade has shifted away from the Kimberley Process (KP) and toward direct company audits via programs like the Responsible Jewellery Council (RJC) and De Beers’ Best Practice Principles (BPP).

More recently, efforts have gone a step further, aiming to account for individual stones in their journey from rough to jewelry. This latter shift is still in its infancy, and traceability programs will become an essential part of a diamond’s identity.

In addition, the idea of what defines an ethically sourced diamond will extend to the identity of the company that mines, manufactures and sells it. When choosing where to buy their jewelry, consumers will be increasingly aware of companies’ corporate social responsibility (CSR) activities.

9. Lab-grown segmentation

A separation between natural and synthetic diamonds is immanent as well. The debate about lab-grown will continue as synthetics find their place in the market — or, as we expect, segment into their own category.

Manufacturers’ and retailers’ current rush into synthetics will reach a saturation point as the market gets crowded. Lab-grown production will continue to grow as technology for making these stones improves, and prices will soften as supply increases — with De Beers emerging as a key price-setter and supplier in the wholesale market.

Demand will also improve, with more synthetics going into lower-value jewelry that used to employ cheap natural diamonds. In that sense, synthetics will play a role in filling the shortfall in supply.

Some retailers with strong branding will have success in bringing synthetics to the engagement-ring segment, but market share in this space will be limited, as the message from the natural diamond trade about synthetics’ ability — or inability — to retain value will ultimately resonate with consumers.

10. Complex category marketing

Consumers will force the diamond industry to make an honest assessment of its trading practices and to relay an authentic message in its marketing.

The biggest challenge facing the trade in the ’20s will be to increase demand. In particular, the industry needs to broaden the range of diamonds that are in demand, reversing the past decade’s trend of concentrating on specific categories.

It will also need to be more open-minded, recognizing the diversity that exists among consumers. Marketing has already become more personalized, and we expect the trade to expand its campaigns accordingly, targeting individual consumers as well as specific groups like the LGBTQ and Hispanic communities.

To accomplish these goals, the industry will need to put a lot more funding into marketing — be it on an individual brand basis, or for category-marketing efforts by the Diamond Producers Association (DPA) or any other mandated body.

Such marketing will be key to navigating the upcoming changes effectively. The diamond trade needs to do better than the $76 billion in retail sales it achieved in 2018. It should be an industry with sales exceeding $100 billion. That’s the gauntlet we’re laying down for the ’20s if the decade is to be worthy of the diamond name.

This article was first published in the October issue of Rapaport Research Report. Click here to subscribe.

Image: Shutterstock

|

|

|

|

|

|

|

|

|

|

Tags:

Alrosa, Avi Krawitz, bitcoin, Chow Tai Fook, De Beers, diamonds, Dpa, Jewelry, lucara, Luk Fook, Martin Rapaport, Rapaport

|

|

|

|

|

|

|

|

|

|

|

|

|