The recent De Beers rough-price hikes were largely expected, but may have been too much for the market to absorb.

RAPAPORT... There were many factors behind the rough-diamond price hikes De Beers reportedly implemented this week. So much so that the move hardly surprised the market, even if it dominated discussions in trading and cutting centers and on online forums. RAPAPORT... There were many factors behind the rough-diamond price hikes De Beers reportedly implemented this week. So much so that the move hardly surprised the market, even if it dominated discussions in trading and cutting centers and on online forums.

Sightholders were a little taken aback by the extent of the increases — an estimated 5% to 12% for 3-grainer and larger goods, and up to 15% for smaller rough. They weren’t expecting such a bold move by the mining company. But on the whole, higher rough prices were anticipated, as noted by this column last week (“The Pressure Is On”).

There, we observed that December through February is generally a busy period for the sector. And since De Beers and Alrosa registered relatively low sales in December, there was some pent-up demand that would be released this month, making it an opportune time to raise prices.

However, seasonality plays only a minor role in influencing market trends. Pricing should rather reflect the balance between supply and demand or indicate that the two are out of sync.

Let’s first look at supply.

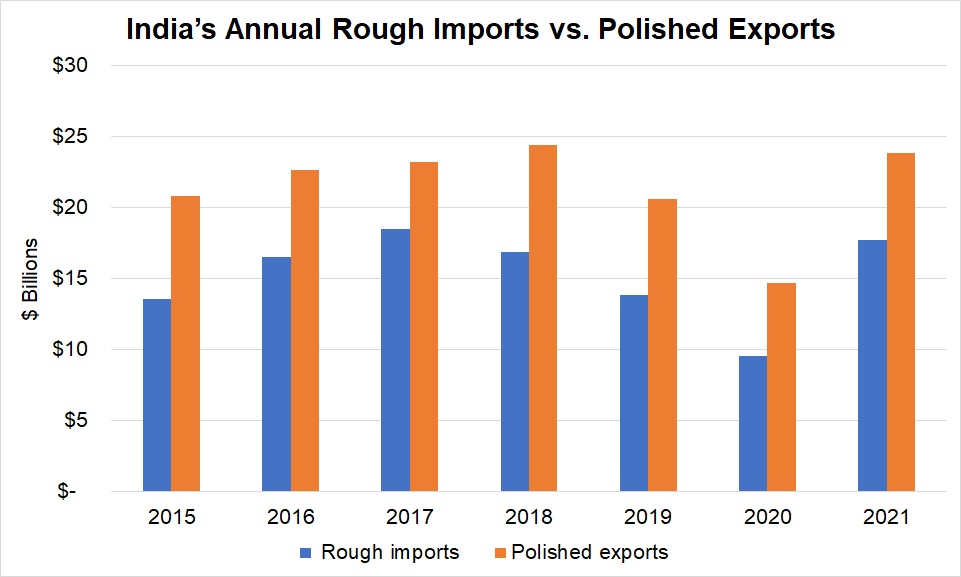

While the two major miners reported lower-than-usual December sales, a lot of rough was in fact sent to cutting factories in India. The spike likely came from other sources and goods bought in previous months but delivered in December. Rough imports to the country rose 20% year on year to $2.1 billion during the month, the Gem & Jewellery Export Promotion Council (GJEPC) reported. That was the highest level in two years, driven by higher prices but also by relatively large volume. When measured in carat terms, December marked the second-highest month for rough imports to India in 2021.

Overall, there was a jump in supply during the fourth quarter, with India’s rough-import volume exceeding 2018 and 2019 levels. And the influx of rough to India for the full year was in line with 2018, which was also a strong period for rough sales. All that is reflected in the polished market as in 2021, India’s polished exports surged to their highest annual total since 2018 (see graph). Furthermore, polished inventory has increased, with the number of stones on RapNet currently at record levels (over 1.7 million diamonds).

Based on monthly data published by the GJEPC.

And yet the biggest complaint among buyers and dealers is that they cannot find goods to replace the inventory they sold during the holiday period. They are reporting shortages in the market of product above 0.70 carats, with excellent cut, symmetry, and polish (triple Ex).

Demand is seen across a broad range of categories, extending from melee, which has seen significant gains in recent months, to dossiers and larger stones. The slight exception is the 0.30-carat category, a size that is most influenced by the Chinese market, where wholesale activity has tapered off ahead of the Lunar festival beginning on February 1 — many buyers have taken early vacations since they didn’t want to buy in such an expensive market anyway.

It is the US that is driving demand. While it is well-known that De Beers does not comment on pricing, the miner would no doubt point to the positive US retail market as a catalyst for this week’s increases. The good news keeps rolling in, with Signet Jewelers reporting Thursday that its holiday sales through November and December rose 30% to $2.4 billion.

There are some concerns that inflation and expected interest-rate hikes might slow the momentum. Those measures raise the cost of living among households, prompting them to prioritize necessities over luxury purchases. Many are also seeing the volatile stock market as an indicator that the momentum will inevitably stall.

For now, though, the industry is riding the wave of robust demand. Its focus has shifted to manufacturers to see how they will react to the recent rise in their rough costs. Dealers note that suppliers have been withholding goods, even when they have orders, as they expect to garner better prices in the coming weeks. With De Beers sharply raising prices — and Alrosa expected to follow suit next week — manufacturers have their excuse to lift polished prices.

But by how much? Will they be able to compensate fully for the extent of the large rough hikes? And would increases in the polished stimulate further spikes in the value of rough down the line? After all, rough should follow trends in polished — not the other way around.

At some point, if prices are pushed by supply rather than pulled by demand, polished buyers will draw the line. They’ll leverage their position and simply not accept suppliers’ high asking price. That’s not something that happens as easily in the rough market. Sightholders are committed to buying a certain percentage of the goods presented at the sights, and they have other factors to consider, such as keeping workers busy and employed.

And there is another new aspect that is influencing the rough segment: the lack of goods on the secondary market where dealers, smaller manufacturers and artisans source rough. And there is another new aspect that is influencing the rough segment: the lack of goods on the secondary market where dealers, smaller manufacturers and artisans source rough.

At the beginning of 2021, De Beers changed its supply policy. It divided sightholders into manufacturers, dealers and retailers to present a more bespoke offering for each category. Alrosa announced an eerily similar move in November.

The idea was to bring greater efficiency to the market by having more goods manufactured sooner. De Beers reduced the number of dealers that flip its boxes to the broader market. It also siphoned more goods for cutting and polishing in Botswana, where it is engaged in ongoing negotiations with the government for a new supply and marketing agreement.

Consequently, it is difficult to find rough despite the large sight, and that is pushing premiums higher on the secondary market, brokers noted this week. The shortage also raises bidding at auctions, which are another avenue for non-sightholders to find goods. That again stimulates higher prices at the sight as De Beers and Alrosa take their cues from the auctions and dealer circuits, too.

It’s a vicious cycle that could overextend the rally. And that would ultimately exert pressure on manufacturing profits. Higher rough prices may have been anticipated this time, but the industry might be better served by a staged approach in smaller increments — as De Beers has implemented in the past. The extent of the price hike was indeed unexpected and may have set in place a dangerously high base from which to start the year.

Image: Avi Krawitz and rough viewed through a loupe. (Ben Kelmer, De Beers)

|